For roughly a year after my birthday in May 2022, I barely paid for food. Friday dinners, weekend brunches, a long string of late-night Zomato orders during deadline weeks, none of it came out of my bank account. The total bill, on the day I first checked the running balance, was ₹21,353 in Zomato Edition Cash sitting in my app. All of it came from one afternoon of careful timing on a credit card that no longer exists in the form I held it. The plan ran for a few hours on one Monday, the credits showed up on the next statement, and the bank itself was never lent a rupee. Here is how it happened, and why it cannot happen again.

The card and the offer

The card was the RBL Zomato Edition Classic. On Zomato spends it ran a generous standing rate, with five percent dining credits at any restaurant on the side and a ₹2,000 milestone bonus once cycle spends crossed ₹2 lakh. Useful enough on its own to keep in the wallet, but not unusual.

The defining feature was the birthday-day boost. On the cardholder's birthday, the specific calendar day, the rate climbed to ten percent on every spend put through the card, with the standard monthly cap suspended for that day. Other days in the same statement cycle earned the standard structure with the standard cap. The boost was a single-day phenomenon, not a month-long one.

This was a documented feature in the card's benefit schedule, not a quiet exploit. RBL was advertising it. The unusual part was simply that they had not bothered to cap it. On my next birthday, every rupee through the card was going to pay back ten percent on whatever I chose to put through it.

The realisation and the plan

NPS Tier 2 was already on my financial calendar for the year. For readers who have not used it: NPS Tier 2 is the unrestricted-withdrawal companion to the locked Tier 1 retirement account. There is no lock-in and no tax-saver hook. Money goes in, sits in PFRDA-managed equity or debt funds at low expense ratios, and can be withdrawn whenever. I was using it that financial year as a flexible parking vehicle for surplus cash, with around ₹2 lakh planned to go in by year-end.

The realisation came the week before my birthday. The eNPS gateway was still accepting credit cards in May 2022, and the merchant code came through clean for Edition Classic rewards. RBL was not excluding NPS contributions from the birthday-day rate. My contribution was already budgeted, the destination was a fund I was happy to hold for years, and the routing fee on eNPS was a fraction of a percent. Putting that contribution through the card on the right day meant ten percent on the full amount, paid out as Zomato credit.

The card was being asked to do exactly one job, on exactly one day. Money was going in either way. All I had to do was time it.

Execution

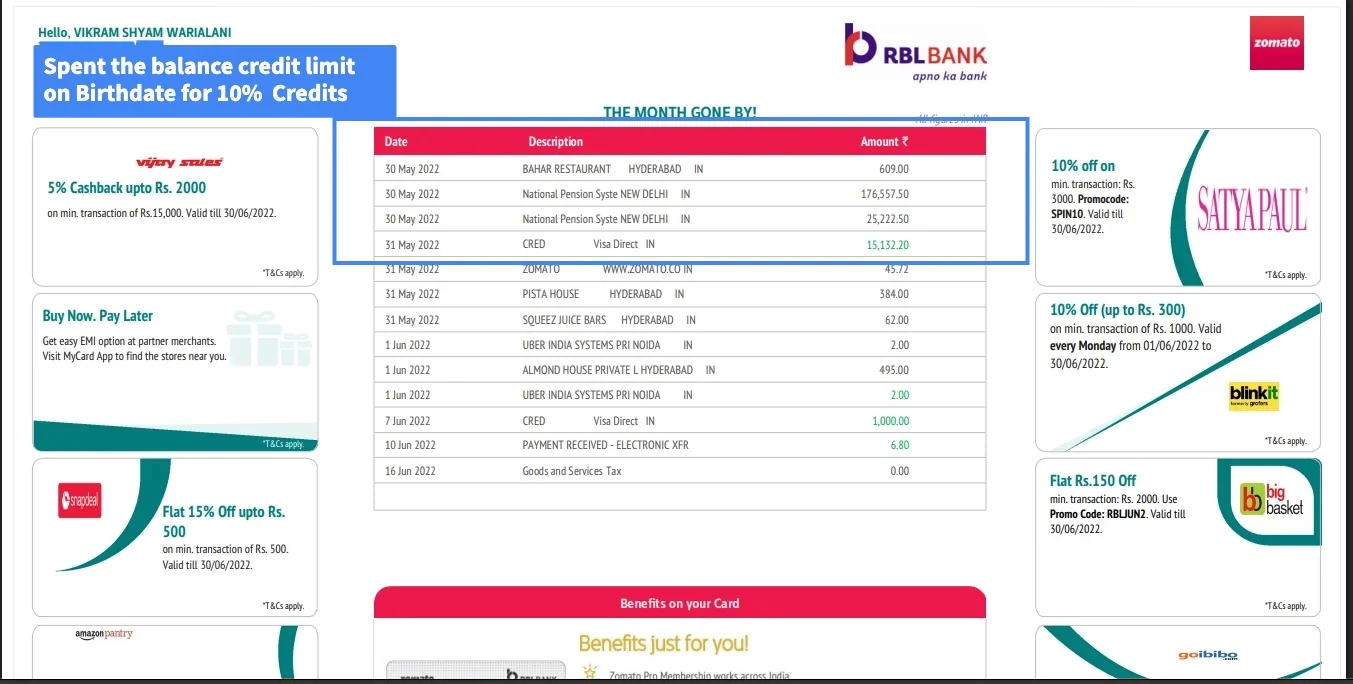

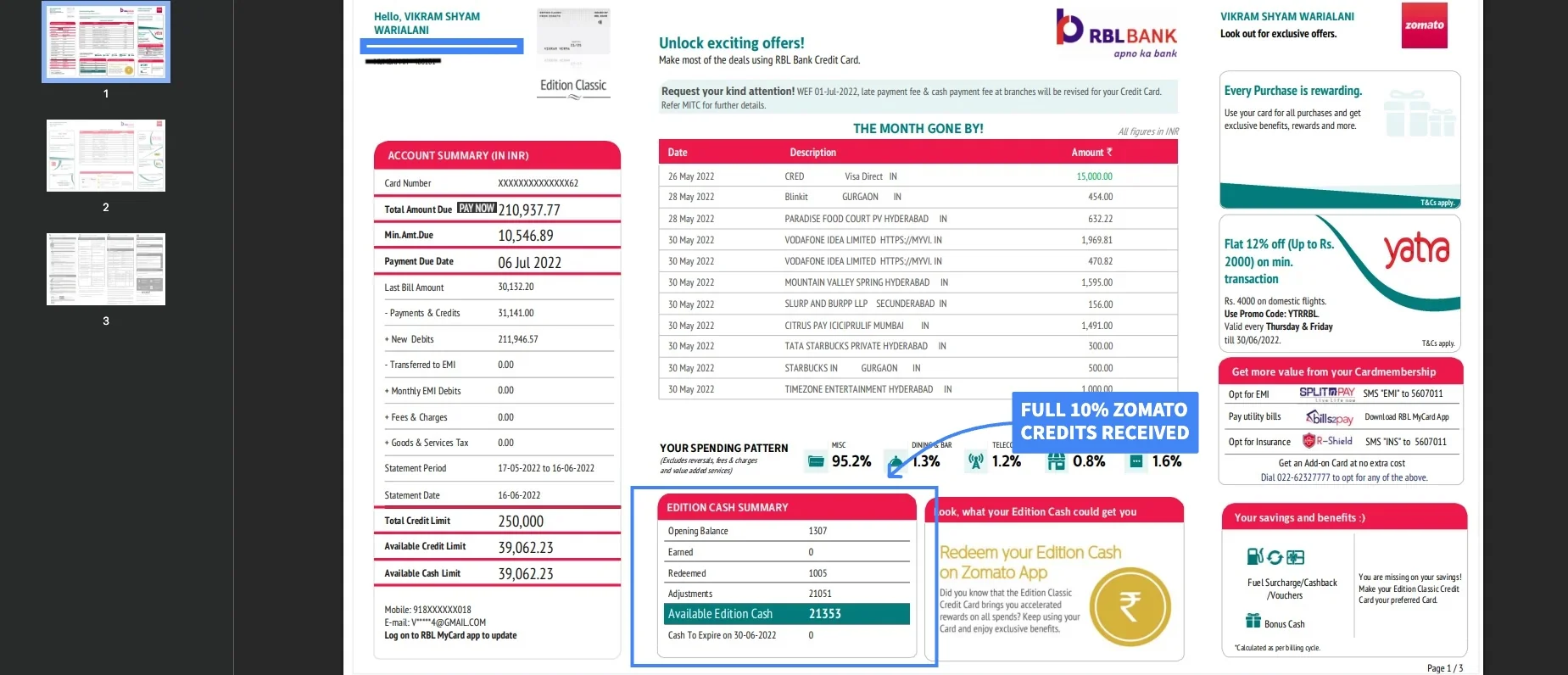

The day was 30 May 2022. I started the morning by clearing the previous cycle's statement balance so the credit limit was fully open. By early afternoon I was logged into the eNPS portal with the card details ready. The first contribution went through without flag: ₹1,76,557.50 to NPS Tier 2, MCC accepted, posted on the Edition Classic. A second followed on the same gateway: ₹25,222.50, also posted clean.

By that point the card was sitting at roughly forty percent of its limit, well below the eighty-percent line where utilisation starts to drag scores. The only other spends on the card that day were a modest dinner at Bahar in Hyderabad to actually celebrate the birthday and a couple of small Zomato orders the same evening. Each of those also rode the ten percent.

The day after, I made a partial pre-payment to the card via CRED's Visa Direct service for ₹15,132.20. That was credit-utilisation hygiene rather than rewards play. With the bill heading toward two lakhs, I wanted the reported balance trending down before the statement cut, even though the rest would clear from savings well before the due date.

The result

The statement closed on 16 June 2022. At the top of the bill, the Edition Cash Summary showed ₹21,353 in available Zomato credits, made up of the ten percent on the birthday-day spends plus a few smaller dining accruals from the cycle. A ₹2,000 milestone bonus for crossing the ₹2 lakh cycle-spend marker landed the following month, taking the running total close to ₹23,000.

The same statement also showed a total amount due of ₹2,10,937.77. I paid that in full from savings before the due date. The NPS Tier 2 balance came back into the picture months later, on its own schedule, with the underlying funds doing what they do regardless of when the contribution went in. The bank was never lent money on this play. The card was a routing mechanism, not a credit instrument.

A year of nearly-free food

The credits sat in the Zomato app, redeemable on food delivery and dine-in, with a usage window that comfortably covered the next twelve months. I drew them down at no particular pace through the second half of 2022 and into early 2023. Friday-night biryanis, weekend brunches with friends, a team lunch from a mid-tier dosa place, the late-night order during a long deadline week. Each time the credit balance ticked down by a few hundred rupees and the bill at checkout went near-zero.

What the redemptions never were was special. There was no bucket-list dining run. There was no celebration meal that justified the build-up. It was just normal eating, on normal evenings, paid for entirely by the timing of one afternoon. By the time the balance ran out in early 2023, I had stopped paying attention to the running total and was caught mildly off-guard the first time a Zomato bill actually charged my card again.

It felt almost too easy.

Why none of this can be repeated

By 2026 the route is a closed door.

NPS contributions via credit card were discontinued at the gateway in August 2022. PFRDA and NSDL together moved the eNPS portal off card payments for both Tier 1 and Tier 2 contributions, citing routing cost. Issuers had already begun reclassifying the NPS merchant code out of the rewards-eligible bucket through mid-2022, and by late that year the route was effectively shut for rewards purposes. A reader trying this play in 2026 will simply find the eNPS portal refuses card payments outright.

The RBL Zomato Edition Classic itself was discontinued shortly after. Later iterations of RBL's Zomato co-branded line moved to capped birthday accruals and reworked benefit structures. The version I held, with the uncapped birthday-day rate, no longer exists.

And the broader era of high-MCC arbitrage on Indian credit cards has been tightened year on year. Wallet-loading routes, education-fee channels, rent-payment apps, fuel-surcharge plays, all have been narrowed by issuers reclassifying the merchant code, capping the rate, or excluding the category outright. The route I used was one specific door. Most of the others on the same corridor have closed since.

What still works

Two things hold up from May 2022, even with the specific route closed.

The first thing is timing. The largest rewards in any given year come from one or two narrow windows where a card's normal cap is suspended or a promotion changes the math, not from the steady base rate. Watching for those windows on the cards already in the wallet is more valuable than chasing the third decimal of a comparison table. Birthday boosts still exist on a few cards, just with caps. Quarterly milestone offers exist on most premium cards. The shape of the play stays the same; the size has shrunk.

The second thing is being clear about where the underlying spend comes from. My ₹2 lakh in May 2022 was already booked for NPS Tier 2 that year. The card structured the timing, not the decision. Any version where the card creates the spend is a losing trade by design, since the ten percent reward is being earned on money that would not have moved otherwise. The arithmetic only holds when the spend was already on the calendar.

The Edition Classic is gone, the NPS card route closed in August 2022, and the broader corridor has been tightened year by year. But the discipline that produced ₹21,353 in May 2022 still applies, on a smaller scale, to whatever the next narrow window turns out to be.

Sources

Frequently asked

Can the NPS Tier 2 via credit card route be used today?

No. NPS contributions through the eNPS portal stopped accepting credit-card payments in August 2022, citing routing cost. The portal now refuses card payments outright for both Tier 1 and Tier 2.

Does the RBL Zomato Edition Classic still exist in the same form?

The card was discontinued shortly after the 2022 changes, and later iterations of RBL's Zomato co-branded line moved to capped birthday accruals. The version with an uncapped birthday-day rate no longer exists.

Are there any cards in 2026 with uncapped birthday or milestone rewards?

Most birthday and milestone offers in 2026 carry per-day or per-cycle caps. Quarterly milestone offers exist on most premium cards, but the headline rate is bounded. The shape of the play is the same as 2022, with the size meaningfully smaller.

How do you avoid creating spend just to chase a milestone bonus?

The arithmetic only holds when the spend was already on the calendar. A ten-percent reward earned on money that would not have moved otherwise is a losing trade, since the underlying transaction is the cost. The card structures the timing of an existing payment, not the decision to make a new one.

Card devaluations, reward maths, and rate changes the day they land.

Follow on X

Reader comments

No comments yet. Share your experience with this card below — the first useful comment helps every reader after you.

Comments are moderated before they appear. Share your real experience with a card — what worked, what didn't, what the bank told you. We don't publish promotional content, referral links, or personal financial details. Keep it useful for other readers.