Updated .

Correction (13 July 2026): an earlier version of this article stated that the Axis Flipkart card carries 4 domestic lounge visits (it has none — they were withdrawn in June 2025), that its fee waiver is ₹2 lakh (it is ₹3.5 lakh), and that the HDFC Millennia pays 2.5% on general online spend (it pays 1%). We have corrected these and re-run the comparison; the Swiggy verdict reverses as a result.

We will cut straight to it. If your top three online merchants are Flipkart, Myntra, and Swiggy, the Axis Flipkart at ₹500 a year beats the HDFC Millennia at ₹1,000 a year. If Amazon is in your top three, or your spending is spread across many merchants, the Millennia wins. The card you should carry is decided almost entirely by where you actually spend, not by which one has the bigger headline number.

The two cards overlap on Flipkart and Myntra, then diverge sharply. Here is how the merchant-level rates compare and why a thousand-rupee fee gap is rarely the deciding factor.

The fee and benefit table

| Metric | Axis Flipkart | HDFC Millennia |

|---|---|---|

| Joining fee | ₹500 | ₹1,000 |

| Annual fee | ₹500 | ₹1,000 |

| Annual fee waiver | ₹3,50,000 spend | ₹1,00,000 spend |

| Top rate | 7.5% Myntra · 5% Flipkart · 5% Cleartrip | 5% on 10 named merchants |

| Secondary rate | 4% on cult.fit, PVR, Swiggy, Uber | — (no middle tier) |

| Default rate | 1% | 1% |

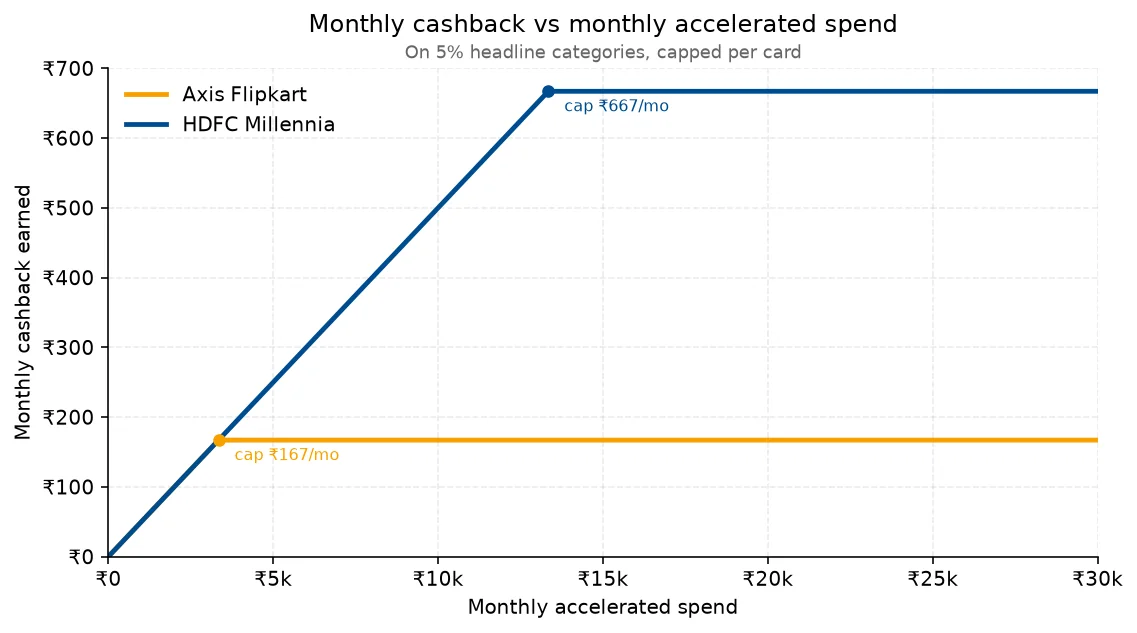

| Cap on the top rate | ₹4,000 per statement quarter, per merchant | 1,000 CashPoints per calendar month |

| Domestic lounges | None | 8 per year (milestone-gated) |

| Min income | ₹3,00,000 | ₹3,00,000 |

Both cards sit at the same income level and both target online shoppers. But the shape of the two reward structures is not the same, and neither card is what its marketing suggests: the Axis Flipkart's fee waiver is far higher than most write-ups claim, and the Millennia has no middle rate at all.

Rates by merchant

Amazon

Only the HDFC Millennia gives 5% on Amazon. The Axis Flipkart is built around the Flipkart group and pays its default 1% on Amazon. For households with significant Amazon spending, this single difference often decides the comparison.

Flipkart, Myntra, and 2GUD

Both cards include Flipkart and Myntra in their accelerated bucket, but not at the same rate and not under the same ceiling.

Axis Flipkart pays 7.5% on Myntra and 5% on Flipkart — each capped at ₹4,000 per statement quarter, separately. That is a generous ceiling: you would need roughly ₹53,000 of Myntra spend or ₹80,000 of Flipkart spend in a quarter to exhaust it. (Note this cap is a 2025 change; the card previously paid unlimited cashback here.)

HDFC Millennia pays 5% but caps the whole 5% category at 1,000 CashPoints per calendar month — a ₹20,000 monthly spend ceiling at the headline rate, across all ten of its merchants combined, not per merchant.

For a household spending less than ₹20,000 a month on Flipkart and Myntra combined, both cards earn the same on these merchants. Above that, Axis Flipkart keeps paying 5% while the Millennia's effective rate falls.

Note that Myntra is the standout here: the Axis Flipkart pays 7.5% on it, the single best rate either card offers on anything.

Swiggy and Zomato

The Millennia wins here, and an earlier version of this article said the opposite. Swiggy and Zomato are both on HDFC's ten-merchant 5% list. The Axis Flipkart pays 4% on Swiggy as a "preferred merchant" and just 1% on Zomato, which is not on its list at all.

For a household ordering food twice a week — say ₹8,000 a month split across both apps — the Millennia's 5% beats the Axis card's blended rate comfortably. Food delivery is a reason to pick the Millennia, not the Axis Flipkart.

PVR, BookMyShow, and entertainment

Axis Flipkart: 4% on PVR, 1% on BookMyShow. HDFC Millennia: 1% on PVR, but 5% on BookMyShow, which is on its ten-merchant list. So it depends where you book — the cinema's own site favours the Axis card, BookMyShow strongly favours the Millennia. Most people book on BookMyShow.

Sony LIV and streaming

HDFC Millennia is one of the few cards naming Sony LIV explicitly in the 5% bucket. Subscriptions are typically small annual amounts, so the absolute rupee impact is minor unless you are paying for multiple OTT services through a single card.

Other online merchants

Neither card has a safety net, and this article previously claimed the Millennia did. There is no 2.5% "other online" tier on the HDFC Millennia — it does not exist in HDFC's current terms. Off-list online spend earns 1%. The Axis Flipkart also pays 1% on anything outside its named merchants.

So on Reliance Digital, MakeMyTrip, BigBasket, Netflix, Adobe, Ajio, direct brand sites and the rest of the internet, the two cards tie at 1%. Neither rewards a spread-out shopper. If your online spending is genuinely scattered, the honest answer is that this pair is the wrong comparison — an all-online 5% card like the SBI Cashback is what you want.

One exception: Tata CLiQ is on the Millennia's 5% list and not on the Axis card's, so it is a Millennia merchant, not a neutral one.

What you get at the airport

The Axis Flipkart no longer has lounge access at all. Complimentary domestic lounge visits were discontinued in the June 2025 revision of the card's terms. A lot of comparison content — including, until this update, ours — still credits it with 4 visits a year. It has none.

HDFC Millennia: 8 domestic lounge visits a year, but milestone-gated — 2 per quarter, unlocked only by spending ₹1 lakh in the previous quarter. If you do not clear that gate, you get nothing either.

So for an occasional flyer this is not "8 versus 4". It is 8-if-you-spend-₹4-lakh-a-year versus zero.

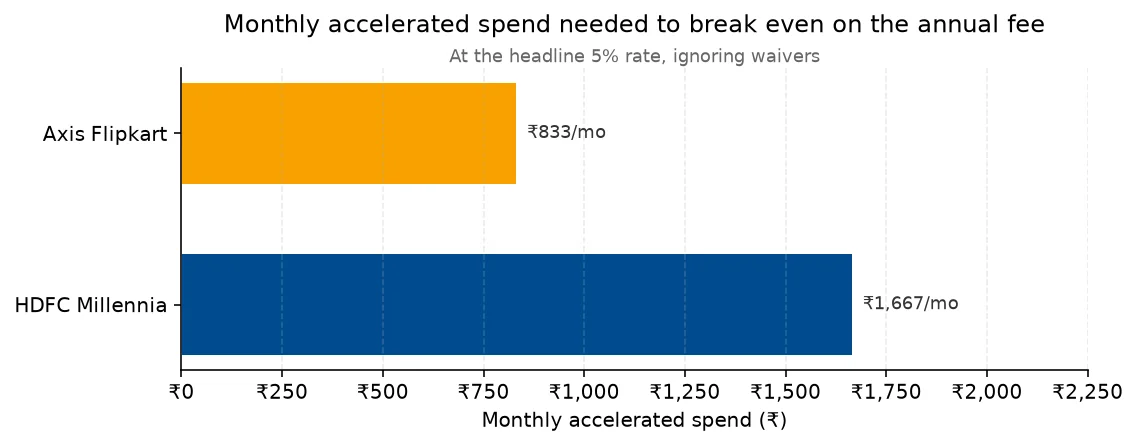

Will you hit the fee waiver?

Axis Flipkart needs ₹3,50,000 of annual spend to waive its ₹500 fee. The Millennia needs ₹1,00,000 to waive its ₹1,000 fee.

That gap is the single most under-reported fact about this pair. ₹3.5 lakh a year is nearly ₹30,000 a month on one card — well beyond a typical online-shopping-only user. The Millennia's ₹1 lakh gate is ₹8,333 a month, which most regular users clear without trying.

So the cheaper-looking card is the one you are far more likely to keep paying for. On a ₹15,000/month spender (₹1.8 lakh a year), the Millennia's fee is waived and the Axis Flipkart's is not — the Axis card starts the year ₹500 down.

The crossover: where the answer flips

Every other comparison of these two cards stops at "it depends on your merchants". Here is the actual number.

Amazon settles it for most people. The Millennia pays 5% on Amazon; the Axis Flipkart pays 1%. That 4-point gap is the largest single difference between the cards, and Amazon is the highest-spend merchant for most Indian online shoppers. If Amazon is in your top two, stop here — take the Millennia.

If you barely use Amazon, the crossover is a Myntra number. On Flipkart the two cards tie at 5%. The Axis card's only real edge is Myntra, where it pays 7.5% against the Millennia's 5% — an edge of 2.5 points.

Now add the fee. Between ₹1 lakh and ₹3.5 lakh of annual spend, the Millennia's fee is waived and the Axis Flipkart's is not, so the Axis card is carrying a ₹500 handicap. To overcome it on its 2.5-point Myntra edge alone:

₹500 ÷ 2.5% = ₹20,000 of Myntra spend a year.

So the crossover is ₹20,000 a year on Myntra — about ₹1,700 a month — provided Amazon is not a meaningful part of your spending. Below that, the Millennia wins on the fee waiver alone. Above it, the Axis Flipkart's Myntra rate starts genuinely paying.

And if you clear ₹3.5 lakh a year, both fees are waived, the handicap disappears, and the Axis Flipkart wins any wallet where Myntra beats Amazon.

Two ceilings worth knowing before you commit: the Millennia's 5% bucket stops paying after ₹20,000 of spend per month across all ten merchants combined. The Axis Flipkart's caps are per-merchant and per-quarter — roughly ₹17,800/month of Myntra and ₹26,700/month of Flipkart before they bind. The Axis card has far more headroom at the top.

Who Should Get Which

Pick the Axis Flipkart if your top merchants are Myntra, Flipkart and Swiggy, and — this is the part that matters — you will genuinely spend ₹3.5 lakh a year on it. The 7.5% on Myntra is the best rate either card offers on anything, and the ₹4,000-per-quarter-per-merchant caps are roomy enough that heavy Flipkart and Myntra shoppers will not hit them. Do not pick it for the lounge access; there isn't any.

Pick the HDFC Millennia if you spend meaningfully on Amazon, Swiggy, Zomato, Uber, BookMyShow or Tata CLiQ — six of its ten 5% merchants that the Axis card either underpays or ignores — or if you will clear ₹1 lakh a quarter and actually use the lounges. It is also the card that does not quietly cost you ₹500 a year, because its waiver gate is a third of the Axis card's.

The Millennia is the better single-card choice for most households, because its 5% list is simply a better map of where Indians spend. The Axis Flipkart is a specialist: superb on Myntra, strong on Flipkart, roomy caps, and nothing else. Carrying both — Axis for Myntra and Flipkart, Millennia for everything else — is a genuinely good setup, but note you will pay the Axis card's ₹500 unless you route ₹3.5 lakh a year through it, which defeats the point of using it selectively.

Run your own numbers

Put the Axis Flipkart and HDFC Millennia side by side for the current fees, caps, and reward rates.

The Millennia also faces a tougher rival on general cashback — HDFC Millennia vs SBI Cashback covers that pair after SBI's April 2026 devaluation.

Sources

Card devaluations, reward maths, and rate changes the day they land.

Follow on X

Reader comments

No comments yet. Share your experience with this card below — the first useful comment helps every reader after you.

Comments are moderated before they appear. Share your real experience with a card — what worked, what didn't, what the bank told you. We don't publish promotional content, referral links, or personal financial details. Keep it useful for other readers.